Aug 04, 2026

What To Do After Tornado Winds Damage Your Roof In Appleton, WI

Key Takeaways

|

Here’s the short answer: yes, roof damage affects your home insurance coverage in NC, but not always in the way you’d expect. Whether your claim is approved, denied, or only partially paid depends on why your roof is damaged, not just that it’s damaged.

That’s not just theory. According to a 2026 report from the U.S. Government Accountability Office, homes in severe or extreme wind-risk areas pay premiums about 58% higher than similar homes with lower wind risk, and parts of North Carolina saw some of the steepest premium increases in the country between 2019 and 2024. Your roof is one of the biggest factors insurers use to price your entire policy.

So before you call your insurance company, let’s walk through what’s actually covered, what gets denied, and how to put yourself in the best position for a fair payout.

In this guide, you’ll learn:

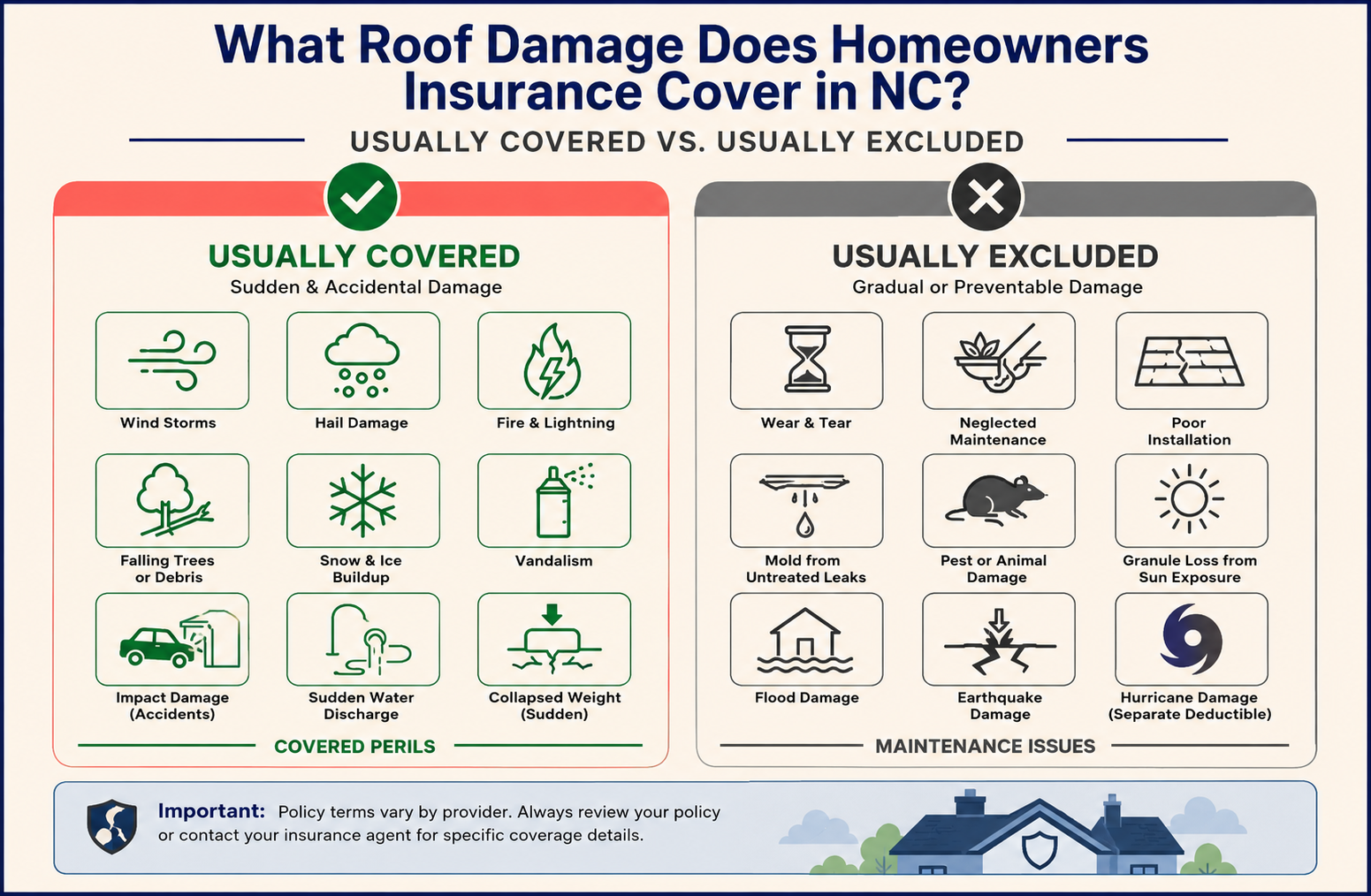

Homeowners insurance in North Carolina typically covers roof damage caused by sudden, accidental events, not damage that builds up slowly over time. Insurers call these “covered perils.”

The table below breaks down what’s usually covered versus what’s usually excluded:

| Usually Covered | Usually NOT Covered |

| Wind damage from storms (missing or lifted shingles) | Wear and tear from natural aging |

| Hail impact damage | Neglected maintenance (ignored leaks, clogged gutters) |

| Fire and lightning strikes | Improper installation or poor workmanship |

| Falling tree limbs or debris | Mold from long-term, untreated leaks |

| Heavy snow or ice buildup causing structural stress | Pest or animal damage |

| Vandalism | Granule loss from sun exposure |

Did You Know? According to NOAA’s National Centers for Environmental Information, North Carolina has experienced 121 separate billion-dollar weather disasters since 1980, and the annual average has jumped from 2.7 events per year historically to 7.4 events per year over just the last five years. That’s why storm-related roof claims are becoming more common across the Piedmont Triad, not less.

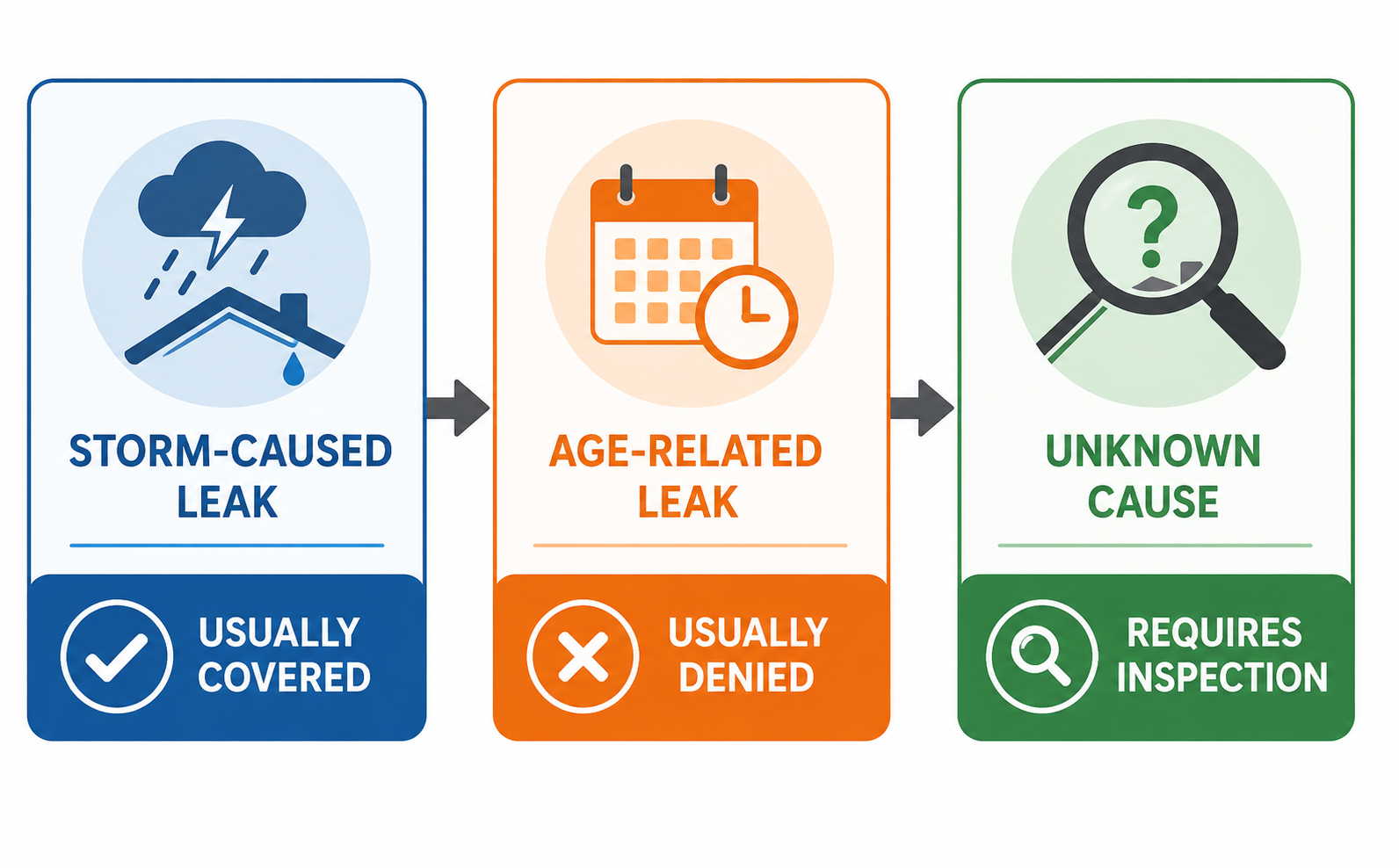

Homeowners insurance covers a leaking roof only when the leak is traced back to a covered peril — like a storm, hail, or falling debris. If the leak is due to age or poor maintenance, it’s typically denied.

Insurers focus on why the roof is leaking, not just that it’s leaking. That distinction decides the whole claim.

Take dated photos the moment you notice damage, and note the exact storm date. Connecting the leak to a specific weather event is the single biggest factor in getting a claim approved.

Whether you or your insurer pays the larger share of a roof repair depends on two things: your deductible and whether your policy pays Actual Cash Value (ACV) or Replacement Cost Value (RCV).

Example: A 15-year-old roof that costs $12,000 to replace might only net $5,000–$7,000 under an ACV policy after depreciation is subtracted

| Feature | ACV Policy | RCV Policy |

| Depreciation subtracted? | Yes | No |

| Typical premium cost | Lower | Higher |

| Payout on older roofs | Significantly reduced | Full replacement cost |

| Best for | Newer roofs, lower premiums | Long-term protection |

Understanding whether your policy provides ACV or RCV coverage can help you estimate your out-of-pocket costs before filing a roof insurance claim.

If you’re stuck with an ACV policy, ask your insurer about a “recoverable depreciation” endorsement. Once repairs are complete and documented, some insurers release the withheld depreciation as a second payment.

Your roof’s age directly shapes what your insurer will pay, whether they’ll renew your policy, and how much you’ll pay in premiums, often before you ever file a claim.

Typical lifespan benchmarks insurers use:

| Roof Type | Expected Lifespan |

| 3-tab asphalt shingles | 15–20 years |

| Architectural shingles | 25–30 years |

| Metal roofing (standing seam) | 40–70 years |

| Wood shake | 20–30 years |

| Tile (clay or concrete) | 50+ years |

As your roof approaches these limits, NC carriers may:

Roof age alone doesn’t determine whether a claim is approved. Insurers also consider the roof’s condition and whether the damage resulted from a covered event or normal wear and tear.

If your roof is approaching the end of its expected lifespan—or you’ve recently experienced severe weather—a professional inspection can provide the documentation needed to assess its condition and identify damage that isn’t always visible from the ground. At Statewide Roofing Specialist, our HAAG-certified drone inspections, GAF Master Elite Certification (top 3% nationwide), and experience completing 10,000+ roofing projects since 2012 help homeowners make informed repair, replacement, and insurance claim decisions. Every inspection is backed by detailed reporting, a 25-year workmanship warranty, and 24/7 emergency service across more than 60 cities in NC, SC, and TN.

Filing a roof damage claim in North Carolina comes down to documenting the damage quickly, promptly notifying your insurer, and obtaining an independent estimate before the adjuster arrives.

After major storms, unlicensed “storm chaser” contractors often show up in affected neighborhoods offering quick fixes. Before signing anything, verify a contractor’s credentials through the NC Licensing Board for General Contractors and confirm they’re established locally. For a full breakdown of what to check after a storm, see our detailed roof damage checklist for NC homeowners.

The best insurance outcome starts long before you ever file a claim — a few habits now can mean the difference between a smooth payout and a drawn-out dispute later.

Our full guide on common roofing problems, warning signs, and repair decisions walks through exactly what to watch for between inspections.

Roof damage affects your home insurance coverage in NC in ways that go well beyond the repair bill itself. Sudden, storm-caused damage is usually covered. Gradual wear and tear almost never is. Your roof’s age, your policy type, and your documentation all determine how much you actually walk away with.

Since 2012, our team at Statewide Roofing Specialist has helped homeowners across Winston-Salem, High Point, Greensboro, and the wider Piedmont Triad navigate exactly this process, backed by GAF Master Elite certification and HAAG-certified storm-damage inspections that insurers trust.

If you’re unsure whether your roof damage qualifies for a claim, call Statewide Roofing Specialist for a free, HAAG-certified inspection before you talk to your insurer.

Yes. Most NC homeowners policies cover storm-related roof damage like wind, hail, and falling debris, as long as the damage is sudden and not caused by neglect or aging.

ACV (Actual Cash Value) subtracts depreciation from your payout based on your roof’s age. RCV (Replacement Cost Value) pays the full cost to replace your roof with new materials, minus your deductible.

Yes. A large roof claim can raise your premium at renewal or lead to non-renewal in high-risk areas, and it stays on your CLUE report for up to seven years.

No. Insurers cover only leaks tied to a specific covered event, such as a storm. Age-related leaks are considered a maintenance issue, not an insurable loss.

Document damage immediately with dated photos, connect it to a specific storm date, get an independent contractor estimate, and consider a HAAG-certified inspection before the adjuster arrives.