Aug 04, 2026

What To Do After Tornado Winds Damage Your Roof In Appleton, WI

Key Takeaways

|

A storm rolls through overnight, and by morning, the damage is impossible to ignore: missing shingles in the yard, a growing water stain on your ceiling, and gutters bent out of shape. The situation feels urgent, but the real question hits quickly: Will your insurance actually cover this?

This uncertainty is more common than most homeowners realize. According to the National Oceanic and Atmospheric Administration, the U.S. experiences dozens of billion-dollar weather disasters each year, many caused by hail, high winds, and severe storms that directly damage residential roofs.

That’s why understanding your coverage before filing a claim matters. In this guide, we’ll break down what storm damage insurance typically covers, why claims get denied, and what steps you should take immediately to protect both your home and your payout.

Not all storm damage is treated the same, and that directly impacts how much your insurer pays. Here’s how the four most common storm scenarios are handled:

Hail can crack shingles, strip away protective granules, and dent metal flashing or gutters. Most standard homeowners’ policies cover hail damage when it’s severe enough to compromise the roof’s function, not just its appearance. In significant hail events, insurers may approve a full replacement rather than patchwork repairs.

| Tip: Check your policy for a separate hail deductible, which is common in storm-prone states and can be much higher than your standard deductible. |

Strong winds can lift, curl, or tear off shingles, and even damage roof edges and ridge caps. Wind damage is typically covered under standard policies, though in some coastal or high-risk areas, a separate wind endorsement may be required. Insurers will often cross-reference official weather data to verify the storm event before approving a claim.

Leaks are covered only when a storm creates an opening that allows water in. If an adjuster determines that a pre-existing crack, worn seal, or aging shingle was the real entry point, and the storm simply made an existing problem worse, the claim is likely to be denied. This is one of the most common friction points in storm claims.

If a storm-toppled tree lands on your roof, the resulting structural damage is generally covered. Thorough photo documentation of the debris and the damage it caused is critical for establishing the storm as the direct cause.

| Note: Depending on your location in NC, SC, or TN, you may need separate wind or hail endorsements. Review your declarations page carefully. |

In North Carolina, roof damage insurance coverage in NC often depends on how well the damage is documented, how quickly the claim is filed, and whether the issue is classified as storm-related or pre-existing. Here are the most common causes:

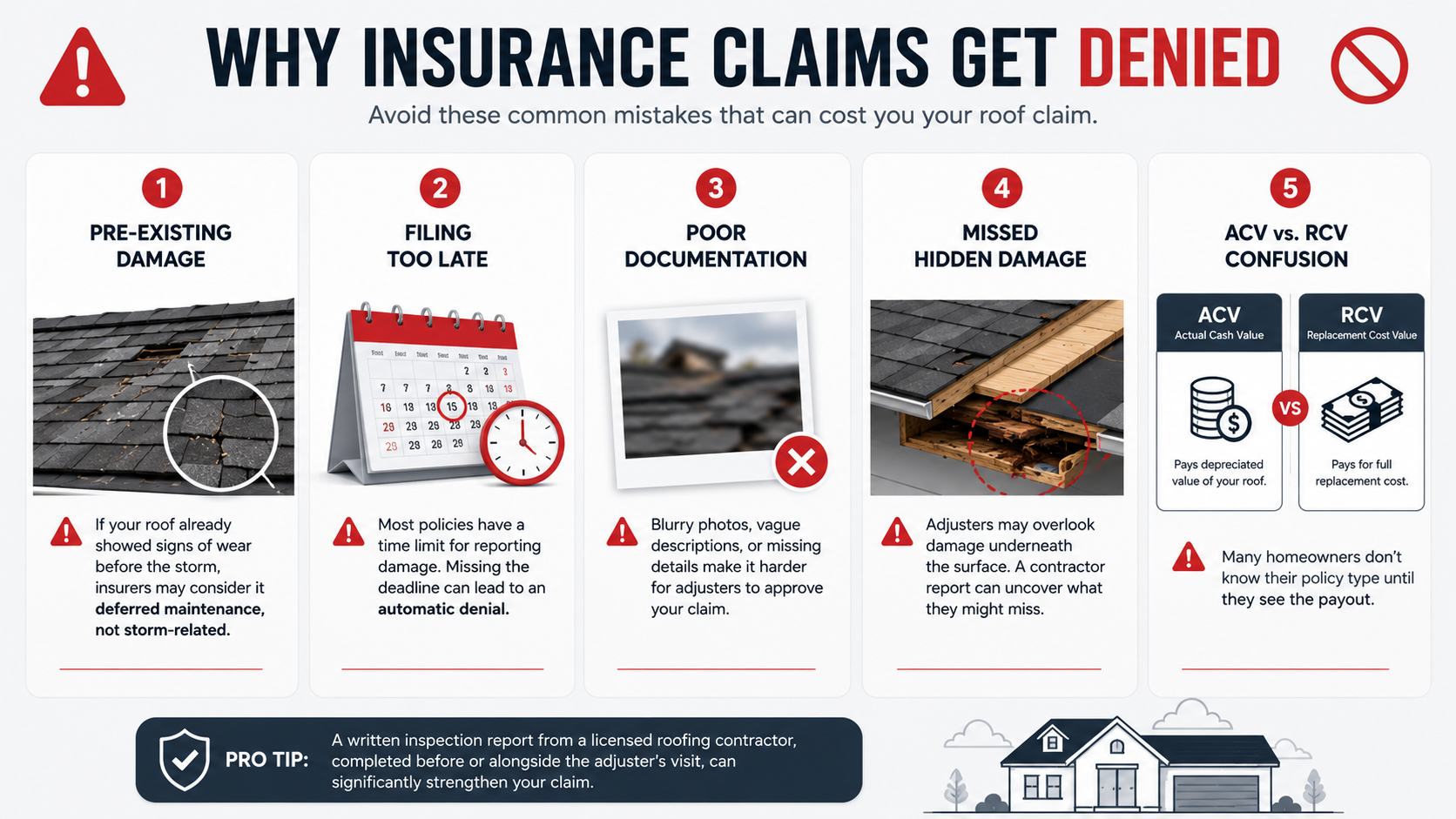

| Pro Tip: A written inspection report from a licensed roofing contractor, completed before or alongside the adjuster’s visit, can significantly strengthen your claim. |

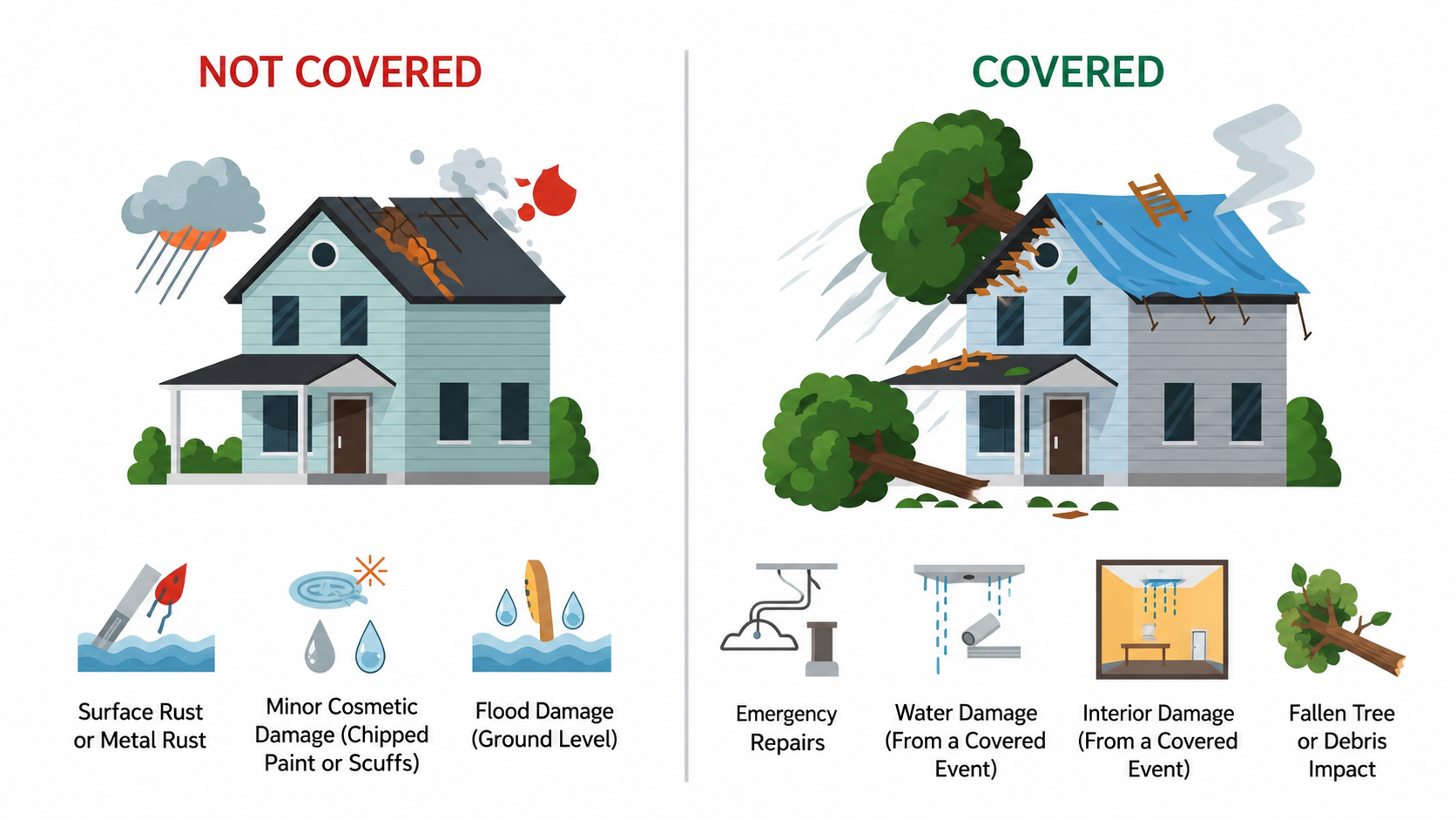

Knowing exclusions upfront prevents surprises after you file. The following are typically not covered under a standard homeowners policy:

What is typically covered includes storm-caused structural damage, debris and fallen tree impact, interior damage that resulted from a storm-created opening, and reasonable emergency repair costs (such as tarping) taken to prevent further loss.

| Important: Flood damage is a major exception in homeowners’ insurance. According to FEMA, most standard policies do not cover flood damage, even though floods can happen anywhere. This is why homeowners often need a separate flood insurance policy through the National Flood Insurance Program (NFIP), which serves over 22,000 communities nationwide. |

Your actions in the hours and days following a storm have a direct impact on whether your claim is approved and on how much it is approved for.

Tip: Keep all receipts related to emergency repairs. These costs may be reimbursable under your policy.

Yes, and this is where many homeowners unknowingly lose coverage they were otherwise entitled to.

Insurance policies include a duty-to-mitigate clause, meaning you’re required to take reasonable action to prevent additional damage after a covered event. If you delay repairs and a small leak develops into rotted decking, damaged insulation, or mold growth, the insurer may argue that the secondary damage resulted from inaction, not the storm, and deny that portion of the claim.

Mold remediation and structural deterioration are frequently excluded when traced to delayed repair rather than to the storm itself. The practical takeaway: address temporary protection immediately, and schedule a professional inspection within days, not weeks, of the storm.

Storm damage coverage isn’t just about whether the storm was severe enough; it depends on your policy type, the condition of your roof before the storm, how well you document the damage, and how quickly you respond. Many denied claims could have been approved with better preparation and faster action.

Your roof is your home’s first line of defense. Don’t let avoidable missteps cost you the coverage you’ve been paying for.

If your home has recently been affected by a storm, Statewide Roofing Specialists offers professional inspections and detailed documentation designed to support your insurance claim and maximize your coverage.

Most homeowners’ insurance policies cover damage caused by sudden events like hail, wind, or falling debris. However, coverage depends on whether the damage is new and storm-related, not due to wear and tear or poor maintenance.

You can strengthen your claim by using:

Timestamped photos and videos

Local weather reports

A professional inspection report

A detailed contractor report is often the strongest evidence when dealing with insurance adjusters.

Common reasons include:

Pre-existing roof damage

Late claim filing

Lack of proper documentation

Minor or cosmetic damage only

Even valid claims can be denied if there isn’t enough proof linking the damage directly to the storm.

It depends on your policy:

RCV (Replacement Cost Value) → covers full replacement

ACV (Actual Cash Value) → pays depreciated value

If the damage affects the roof’s functionality (not just appearance), insurers are more likely to approve a full replacement.

Avoid climbing on the roof

Document all visible damage

Prevent further damage (tarp if needed)

Schedule a professional inspection

File your claim quickly

Taking action within the first 24–48 hours can significantly impact your claim approval.